{kind=link}

What if a loan’s main job is to build your credit – not to give you cash today?

Credit builder loans do exactly that: the lender locks the money in a savings account, you make fixed monthly payments, and those payments get reported to the credit bureaus.

Think of it as forced savings plus proof you pay on time.

This post explains how they work, who they help, and the key trade-offs, like fees, eligibility checks, and why a missed payment can hurt more than help.

Read on to learn whether one makes sense for you.

Understanding the Purpose and Function of a Credit Builder Loan

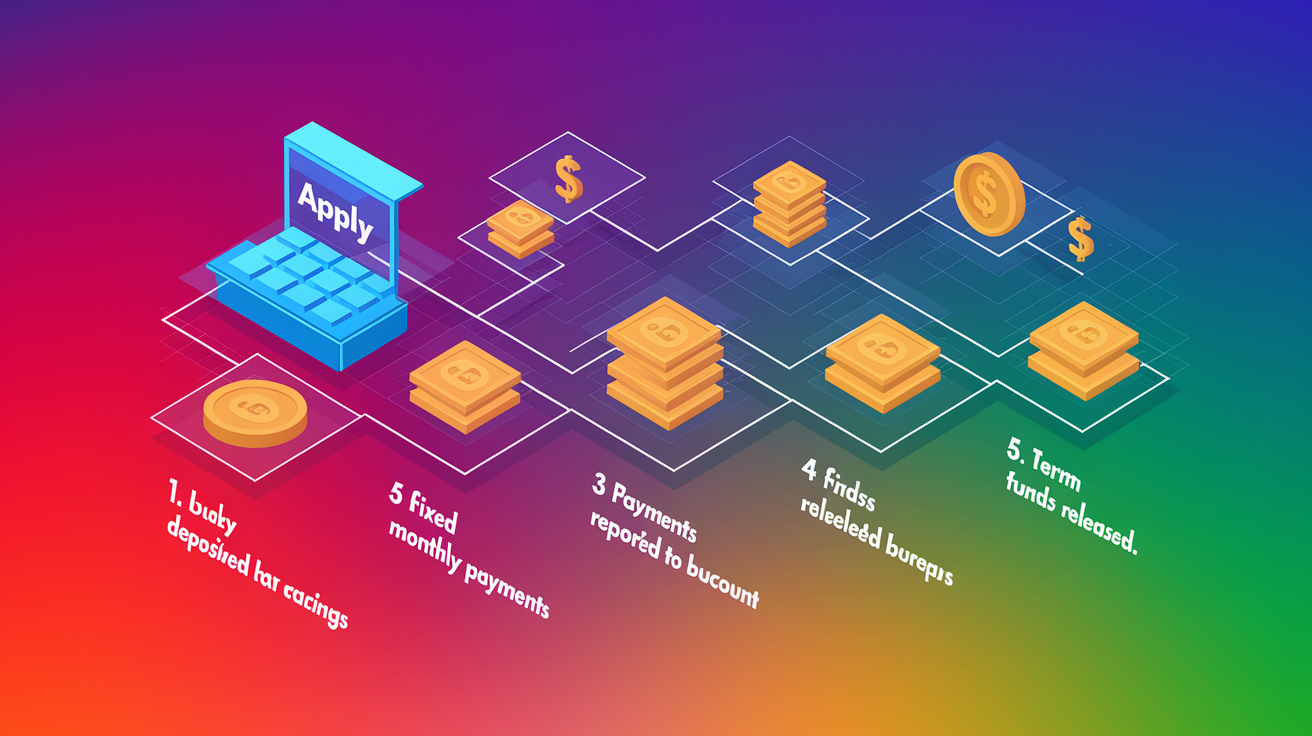

A credit builder loan is a small installment loan built to help people with zero credit or bruised credit establish a solid payment track record. Here’s the twist: you don’t get any money upfront. The lender stashes the loan amount (usually $300 to $1,000) into a locked savings account or certificate of deposit. You make fixed monthly payments over 6 to 24 months, and the lender reports those payments to the major credit bureaus every month. Once you’ve paid off the entire loan, they hand you the funds.

Why lock up the money? It protects the lender and makes qualification easier, even if you’ve never borrowed before or made mistakes in the past. Since the cash stays locked until you finish paying, the lender faces almost zero risk. This setup lets people who can’t get approved for traditional credit still prove they can handle monthly payments. When the term ends and you’ve made every payment on schedule, the lender releases the balance. You get forced savings plus proof you’re creditworthy.

Credit reporting is what makes this thing valuable. Lenders report your monthly payment activity to Experian, Equifax, and TransUnion. Those bureaus use the data to calculate your credit scores. Payment history accounts for 35% of the FICO scoring model most lenders rely on. Each on-time payment adds a positive mark to your credit file, gradually building the kind of track record lenders want to see when you apply for a car loan, apartment, or credit card. Miss a payment by 30 days or more? It’ll likely be reported as a negative mark that can stick around for up to 7 years. Consistency matters.

How a Credit Builder Loan Works Step-by-Step

The mechanics are simple once you get the basic structure. After approval, the lender doesn’t hand you cash. They place the loan amount in a savings account, certificate of deposit, or another interest-bearing account you can’t touch. You make monthly payments like any other loan. Those payments cover the principal plus any interest or fees the lender charges. The lender reports each payment to the credit bureaus. At the end of the term, you get the money back, minus any interest you paid.

Interest and fees vary by lender. Some credit unions return part of the interest or dividends at the end. Others keep it to cover administrative costs. Quick example: a $1,000 loan at 5% APR over 12 months costs roughly $86 per month. You’ll pay about $27 in total interest. After the final payment clears, you receive $1,000 back. That $27 is what you paid to build credit and create a small savings cushion. Other lenders charge higher rates or tack on origination fees, so compare before you commit.

Here’s the process from start to finish:

- Apply with the lender and get approved based on income, bank history, or other criteria (rarely a traditional credit check).

- The lender deposits the loan amount into a locked savings or certificate account in your name.

- You begin making fixed monthly payments according to the agreed schedule, usually over 6 to 24 months.

- The lender reports your payment activity to at least one credit bureau each month, ideally all three.

- You complete the loan term by making every payment on time, including the final payment.

- The lender releases the funds to you. You receive the principal (sometimes with a portion of interest or dividends).

Typical loan amounts range from $300 at the low end to $1,000 or occasionally $3,000 at the high end. 12 months is the most common term length. Shorter 6-month terms exist but limit how many on-time payments you can report. 24-month terms give you more credit-building months but tie up the funds longer. The key benefit happens every month when the lender reports your payment. Each report adds a fresh installment payment to your credit history, which is exactly what people with thin or damaged files need most.

Credit Builder Loan Impact on Your Credit Score

Payment history is the single most important factor in your FICO score, accounting for 35% of the calculation in FICO Score 8 (the model many lenders still use). A credit builder loan gives you a predictable way to add positive payment history month after month. Each on-time payment shows you can manage debt responsibly. Over time those marks accumulate to form a reliable track record. If you had no credit file before, this product creates one. If you had past negatives, consistent new positives help balance the picture.

The flip side is equally strong. If you miss a payment by 30 days or more, the lender will likely report it as late to the bureaus. That late payment can stay on your report for up to 7 years. One or two late marks can erase months of progress, drop your score significantly, and make it harder to qualify for other credit. This is why affordability matters so much. Signing up for a payment you can’t consistently make will hurt you more than help you.

Most reputable lenders report to all three major credit bureaus: Experian, Equifax, and TransUnion. Reporting to all three ensures your payment history shows up on every version of your credit report. No matter which bureau a future lender checks, they’ll see your track record. If a lender only reports to one or two bureaus, you’re leaving gaps that could cost you when you apply elsewhere.

Here’s what happens to your credit profile when you use a credit builder loan responsibly:

- Establishes installment loan history if you’ve never had one, diversifying your credit mix (10% of FICO score).

- Adds consistent on-time payment marks each month, the most heavily weighted scoring factor.

- Increases the length of your credit history gradually as the account ages and remains on your report after payoff.

- Shows active credit usage, which scoring models prefer over completely empty files.

- Provides proof of financial responsibility that future lenders can verify when reviewing your application.

The impact isn’t instant. Credit scores improve gradually as your payment history grows. Expect to see modest gains after a few months of on-time payments, with more meaningful improvement after six months or more. The longer you maintain the account and the more months you report, the stronger the signal to lenders that you’re a safe bet.

Eligibility Requirements for a Credit Builder Loan

Most lenders offering credit builder loans don’t require a minimum credit score. The whole point of the product is to help people who lack credit or have damaged credit, so traditional credit checks are often skipped or given less weight. Instead, lenders may review your banking history using systems like ChexSystems, which tracks bounced checks, account closures, and other red flags. If you have a history of overdrafts or unpaid bank fees, it can still disqualify you even without a credit check.

Lenders focus on your ability to afford the monthly payment. You’ll need to provide proof of income (pay stubs, tax returns if you’re self-employed, or bank statements showing regular deposits). Some lenders ask for details about your current housing payment, other loan balances, and checking or savings account balances to verify you can handle another bill. The application is simpler than a traditional loan, but you still need to show that your income covers your expenses plus the new payment.

| Requirement | What Lenders Look For |

|---|---|

| Income verification | Pretax monthly income, pay stubs, or tax returns (self-employed) |

| Bank history | No recent bounced checks, overdrafts, or closed accounts for cause |

| Identification | Valid government ID and Social Security number for reporting |

| Housing & debt details | Current rent or mortgage, other loan balances, and monthly obligations |

Approval is usually faster and easier than a traditional unsecured loan because the lender holds the funds as collateral. Many applications are approved within a few business days. Some online lenders give instant decisions. Credit unions may require membership before you apply, which can take an extra day or two and costs a small deposit (often $5 to $25 or a donation to a partner charity). Once approved, you can typically start making payments right away. The lender begins reporting to the bureaus immediately or after the first payment clears.

Costs, Interest Rates, and Fees in Credit Builder Loans

Interest rates and fees vary widely depending on the lender and your financial profile. Borrowers with thin or poor credit typically face higher rates because lenders price in the perceived risk, even though the funds are secured. APRs can range from around 5% at credit unions to 15% or more at online lenders. Some products charge fees on top of interest. Always check the total cost (principal plus interest plus any fees) before you agree to the loan.

Some lenders charge an origination fee upfront. It’s a one-time cost deducted from the loan amount or added to your balance. Others may charge late fees if you miss a payment. A few impose prepayment penalties if you pay off the loan early, though early payoff is usually allowed. A handful of credit unions and community lenders return a portion of the interest or dividends to you at the end of the term, which reduces your effective cost. Read the terms carefully to know exactly what you’ll pay.

Here’s a breakdown of common costs to watch for:

- Interest (APR): The annual percentage rate applied to your loan balance. Total interest depends on the rate, loan amount, and term length.

- Origination fee: A one-time charge, sometimes a flat dollar amount or a percentage of the loan, that covers processing.

- Late payment fee: Charged if you miss a payment deadline. Can range from $10 to $35 or more.

- Prepayment penalty: A fee for paying off the loan early (uncommon but check the fine print).

- Membership fee (credit unions): A one-time deposit to join, typically $5 to $25, which may be refundable or stay in a share account.

- Monthly maintenance or service fees: Rare, but some lenders tack on administrative costs each month.

Be cautious of APRs above 36%. Consumer advocates and state lending laws often use that threshold as a warning sign for predatory or high-cost credit. If you’re quoted a rate significantly above that, compare other lenders or consider alternatives like a secured credit card or a lending circle. The goal is to build credit affordably. Paying excessive fees and interest erodes the financial benefit and makes it harder to stay current on payments.

Pros and Cons of Using a Credit Builder Loan

Credit builder loans are designed for a specific purpose. They work well when used correctly. The main benefit is simple: they create a structured way to build installment payment history when you can’t qualify for traditional credit. You make fixed monthly payments, the lender reports them to the bureaus, and at the end you get your money back plus proof that you’re creditworthy. For people with no credit score or a thin file, this is one of the most accessible entry points into the credit system.

The drawbacks are equally important. You don’t get access to the funds up front, so if you need money for an emergency or expense, this product won’t help. You’re essentially paying interest and fees to borrow your own money, which can feel backward. And if you miss payments, you’ll harm your credit instead of building it. Late payments stay on your report for years and can drop your score significantly.

Pros:

- Builds installment payment history even with no existing credit or poor credit

- Easier to qualify for than traditional unsecured loans

- Forced savings (funds are returned to you at the end of the term)

- Reports to credit bureaus monthly, adding positive marks to your file

- Low risk to the lender, which means more flexibility for borrowers

Cons:

- Funds are locked and inaccessible until the loan is paid off

- You pay interest and possibly fees to borrow money you can’t use

- Missed or late payments damage credit and may be reported for up to 7 years

- High APR loans reduce the financial benefit and increase total cost

- Limited credit-building impact if the lender doesn’t report to all three bureaus

This product makes the most sense if you can afford the payment comfortably, you don’t need the cash immediately, and you’re committed to making every payment on time. It’s not a replacement for emergency savings or a solution if you’re already struggling to cover basic bills. Adding another monthly obligation increases the risk of default and backfire.

Where to Get a Credit Builder Loan

Credit unions are the most common source. Many credit unions offer credit builder loans as a member service, with lower rates and more flexible terms than commercial lenders. Joining a credit union typically costs $5 to $25, either as a one-time membership fee or a small deposit into a share savings account. Some credit unions waive the fee if you donate to a partner charity. Once you’re a member, you can apply for the loan and often get approved quickly if your income and bank history check out.

Community banks and community development financial institutions (CDFIs) also provide these loans, often as part of financial inclusion programs. These lenders focus on underserved populations and may offer interest-free or very low-rate loans with flexible repayment terms. Online lenders have entered the market too, offering faster applications and approvals, though interest rates and fees can be higher. Lending circles (small peer groups that issue interest-free social loans) are another option, typically facilitated by nonprofit organizations that report payments to the bureaus.

Here’s a quick overview of each source:

- Credit unions: Member-owned, often lower rates, may return dividends. Require membership (usually $5 to $25).

- Community banks: Local focus, flexible underwriting, may offer financial coaching alongside the loan.

- Online lenders: Fast application and approval, higher APRs and fees in many cases, wide accessibility.

- Lending circles: Community-based, often interest-free, payments reported to bureaus, facilitated by nonprofits like Mission Asset Fund or local CDFIs.

Before choosing a lender, compare three key factors: total cost (interest plus all fees), bureau reporting (look for lenders that report to all three), and term flexibility. Ask whether the lender returns any interest or dividends at the end. Confirm there are no hidden fees. If two lenders offer similar loan amounts and terms, pick the one with the lower APR and the most transparent fee structure. The difference of a few percentage points can save you $20 or more over the life of the loan. Reporting to all three bureaus maximizes the credit-building benefit.

Comparing Credit Builder Loans to Alternatives

Credit builder loans aren’t the only tool for building credit, and they’re not always the best fit. Depending on your situation, other products may give you more flexibility, faster access to funds, or better long-term value. The right choice depends on whether you need cash now, how much you can afford to deposit or pay monthly, and what kind of credit history you want to build.

Secured Credit Cards

A secured credit card requires a refundable security deposit, typically $200 to $2,000, which becomes your credit limit. You use the card for purchases, pay the balance each month, and the issuer reports your payment activity to the bureaus. Unlike a credit builder loan, you get immediate access to the credit line and can use it for everyday expenses. The deposit is refunded when you close the account in good standing or upgrade to an unsecured card. Secured cards are a good option if you need revolving credit (the kind used for building a strong credit mix) and can handle the temptation to overspend.

Authorized User Accounts

If someone with good credit adds you as an authorized user on their credit card, the account’s payment history may transfer to your credit report. You don’t have to make payments or even use the card. You’re simply piggybacking on their responsible behavior. This approach works best when the primary cardholder has a long history of on-time payments and low credit utilization. The downside is you have no control. If the primary user misses payments or maxes out the card, it can hurt your credit too. Not all issuers report authorized users to all three bureaus, so confirm before relying on this method.

Lending Circles

Lending circles are social loan programs where a small group of people each contribute a set amount monthly, and members take turns receiving the pooled funds. A facilitating nonprofit reports payments to the credit bureaus, so you build credit while participating. These programs are often interest-free, making them one of the most affordable credit-building tools. The catch is availability. Lending circles are typically offered by community organizations and may have limited spots or geographic restrictions. Mission Asset Fund and similar groups run these programs nationwide.

Rent/Utility Reporting Tools

Free services like Experian Boost let you add rent, utility, cellphone, and some streaming subscription payments to your credit file instantly. The data is pulled from your bank account or payment history and added to your Experian credit report, which can raise your FICO score if the payments are on time. The boost is limited to Experian unless you use a paid service that reports to multiple bureaus. Results vary. Some people see meaningful gains, others see little change. It’s a zero-cost, zero-risk option worth trying if you’re already paying those bills on time every month.

| Option | Deposit Required | Upfront Access to Funds | Builds Credit? |

|---|---|---|---|

| Credit builder loan | None | No | Yes, via installment payment history |

| Secured credit card | $200–$2,000 | Yes, as credit limit | Yes, via revolving credit history |

| Authorized user | None | No (unless given card) | Yes, if issuer reports authorized users |

| Rent/utility reporting | None | N/A | Yes, limited to reported bureaus |

How to Apply for a Credit Builder Loan

Start by checking your credit report. You’re entitled to one free report from each of the three major bureaus (Experian, Equifax, and TransUnion) every year through AnnualCreditReport.com. Reviewing your report helps you understand where you stand and identify any errors that could affect your application. If you find mistakes, dispute them before you apply so lenders see the cleanest version of your file.

Next, compare lenders. Look for institutions that report to all three bureaus and offer transparent fee structures. Credit unions often have the best combination of low rates and member benefits, but online lenders may approve you faster if you need to start building credit immediately. Read customer reviews and check complaint records with the Better Business Bureau or your state’s financial regulator to avoid predatory lenders or hidden fees.

Gather the required documents before you submit your application. You’ll need a government-issued ID, your Social Security number, proof of income (pay stubs or tax returns), details about your current bank accounts, your housing payment amount, and information about any other loans or debts you’re repaying. Having everything ready speeds up the approval process and reduces the chance of delays.

Here’s the step-by-step process once you’re ready to apply:

- Check your credit report at AnnualCreditReport.com and review for errors or issues.

- Research and compare lenders for APR, fees, bureau reporting, and loan terms.

- Gather required documents: ID, SSN, proof of income, bank statements, housing payment info, and debt balances.

- Submit your application online, in person, or over the phone, depending on the lender.

- Review and sign the loan agreement after approval, confirming the APR, fees, payment schedule, and bureau reporting.

- Make your first payment on or before the due date, then continue on-time payments for the full term.

Approval times vary. Some online lenders give instant or same-day decisions. Credit unions and community banks may take a few business days to review your application and verify income. Once approved, you’ll sign a loan agreement that spells out the payment amount, due dates, interest rate, fees, and term length. Read it carefully and keep a copy for your records. After the first payment clears, the lender begins reporting to the bureaus. Your credit-building journey starts.

Timeline and Expected Results from a Credit Builder Loan

Credit improvement is gradual, not instant. Most credit builder loans run for 6 to 24 months. Meaningful score gains typically require several months of consistent on-time payments. If you start with no credit score, you may see a score appear within a few months as the bureaus gather enough data to calculate one. If you already have a score but it’s low due to past negatives, new positive payments help balance your history over time, though old negatives won’t disappear until they age off your report.

The longer you maintain the account and the more months you report, the stronger the impact. A 6-month loan gives you six on-time payment marks, which is a good start but limited. A 12-month loan doubles that. A 24-month loan provides two years of positive installment history. After the loan is paid off and closed, it remains on your report as a closed account in good standing, which continues to contribute to your credit age and payment history for years.

Here’s what to expect during and after the loan term:

- First 1 to 3 months: Lender reports your account and first payments. Score may rise modestly or stay flat as bureaus gather data.

- Months 3 to 6: Multiple on-time payments accumulate. Noticeable score improvement if you had a thin file or recent negatives are being balanced.

- Months 6 to 12: Consistent payment history solidifies. Lenders reviewing your report see reliable installment behavior.

- After payoff: Closed account in good standing stays on your report for up to 10 years, continuing to support your credit age and payment history.

Results depend on your starting point, the rest of your credit profile, and whether you maintain perfect payment timing. If you miss a payment or pay late, the benefit is reduced and the negative mark can offset months of progress. If you have other active accounts with on-time payments, the credit builder loan reinforces that pattern. If it’s your only account, it carries more weight and has a bigger impact on your score.

Frequently Asked Questions About Credit Builder Loans

Does paying off a credit builder loan early help or hurt my credit?

Paying off the loan early is usually allowed, and it gives you faster access to the funds. The downside is it reduces the number of on-time payments reported to the bureaus, which limits the credit-building benefit. For example, if you have a 12-month loan but pay it off in 6 months, you only get six payment marks instead of twelve. If your goal is to maximize credit impact, stick to the full term and make every scheduled payment.

What happens if I miss a payment?

Missing a payment can trigger a late fee. If the payment is more than 30 days overdue, the lender will likely report it to the credit bureaus. That late mark can stay on your report for up to 7 years and drop your score significantly. If you realize you’re going to miss a payment, contact the lender immediately. Some will work with you to adjust the due date or waive the fee if you communicate early.

Can I get a credit builder loan with no income?

Most lenders require proof of sufficient income to afford the monthly payment, so qualifying with no income is difficult. Some lenders may accept alternative documentation, like regular deposits from government benefits, a co-signer with income, or proof of savings that can cover the payments. If you have no income and no co-signer, a secured credit card or becoming an authorized user may be more realistic options.

How long should I keep records of my payments?

Keep copies of your loan agreement, payment receipts, and any correspondence with the lender until at least a year after the loan is paid off and you’ve confirmed the account appears correctly on your credit report. If there’s ever a dispute about whether a payment was made or reported, those records are your proof. Digital copies stored securely are fine. Just make sure they’re backed up.

Do all lenders report to all three credit bureaus?

No. Some lenders report to only one or two bureaus, which limits the visibility of your payment history. Before applying, confirm the lender reports to Experian, Equifax, and TransUnion. Reporting to all three ensures your credit-building effort shows up no matter which bureau a future lender checks.

Will a credit builder loan remove negative marks from my credit report?

No. A credit builder loan adds positive payment history, but it doesn’t erase past late payments, collections, or other negatives. Those items remain on your report for up to 7 years (or longer for certain items like bankruptcies). The new positive payments help balance your profile over time, which can gradually improve your score, but old negatives only disappear when they age off or are successfully disputed as errors.

Final Words

You now know the basics: what a credit-builder loan is, how the held savings and monthly payments work, and how those payments get reported to the credit bureaus.

Remember the practical steps: compare fees and APRs, check who reports to the three bureaus, gather ID and income papers, and make every payment on time. Watch for upfront fees and locked funds until payoff.

If you’re still asking what is a credit builder loan, it can be a low-cost, low-risk way to build payment history and improve your score over months. Start small and stay consistent.

FAQ

Q: Is a credit builder loan a good idea?

A: The credit builder loan is a good idea when you need to build or repair credit and can make on-time payments for 6 to 24 months; it reports payments to bureaus, but funds stay locked until payoff.

Q: How much can I get with a credit builder loan?

A: How much you can get with a credit builder loan usually ranges from $300 to $1,000, with some lenders offering slightly more; term lengths commonly run 6 to 24 months.

Q: Can you get a loan on SSDI?

A: You can get a loan on SSDI because many lenders accept Social Security disability as income, but approval depends on lender rules, required documents, and your income-to-debt situation.

Q: Can you be denied for a credit builder loan?

A: You can be denied for a credit builder loan for reasons like insufficient income, bad bank-history (ChexSystems), missing ID or income documents, or not meeting lender membership requirements.