{kind=link}

Think paying off a collections account will instantly raise your credit score? Not always.

It sometimes helps fast, and sometimes it barely moves the needle depending on which scoring model a lender uses (FICO 8 versus FICO 9, FICO 10, or VantageScore 3.0/4.0), how recent the debt is, and whether you negotiate pay-for-delete.

This post shows which models give you a real bump, how long updates usually take, and the practical steps to actually improve your credit after you clear a collection.

How Paying Off a Collections Account Affects Your Credit Score

Sometimes it does, sometimes it doesn’t. If the lender’s using a newer scoring model like FICO 9, FICO 10, VantageScore 3.0, or VantageScore 4.0, paying off that collection can actually boost your score. Those models either ignore paid collections completely or give them way less weight. But if you’re dealing with an older model like FICO 8, you might not see any movement at all because FICO 8 treats paid and unpaid collections exactly the same. What happens depends entirely on which model generates the number your lender actually looks at.

Newer models reward you for clearing debt. They’re built on the idea that someone who pays what they owe is a safer bet than someone who leaves it sitting there. FICO 9 and FICO 10 toss paid collections out of the calculation completely and go easier on unpaid medical debt. VantageScore 3.0 and 4.0 take it even further, ignoring all paid collections and all medical collections whether you’ve handled them or not. FICO 8, which a lot of lenders still lean on, offers no such break. It keeps factoring that paid collection into your score just like it did before.

You’re more likely to see your score jump after paying if:

- The lender’s pulling FICO 9, FICO 10, VantageScore 3.0, or VantageScore 4.0

- The collection isn’t medical and it’s over $500

- Your credit file doesn’t have a bunch of other problem marks

- The debt’s fairly recent and still racking up interest or fees

- You’re applying for a mortgage, since mortgage lenders are shifting to FICO 10T and VantageScore 4.0 by the end of 2025

Even when your score stays flat, paying that collection stops lawsuits, kills ongoing interest and fees, keeps the debt from getting sold to yet another collector, and improves how future lenders see you when they review your full report instead of just the number. A lot of lenders won’t approve you until collections are paid, score aside.

Differences Between Credit Scoring Models and How They Treat Paid Collections

Credit scores aren’t all the same, and lenders pick different models depending on what kind of credit you’re after. Knowing which model a lender uses helps you figure out whether paying a collection will lift your score or just mark it resolved without changing anything.

FICO 8

FICO 8 doesn’t give you any credit for paying collections. Any collection over $100 hurts your FICO 8 score for up to seven years from the date you first fell behind, whether you pay it or not. Paying changes the status to “paid,” sure, but FICO 8 keeps penalizing it as a serious negative mark. Auto lenders and plenty of credit card companies still use FICO 8, so don’t expect an immediate bump after you settle up.

FICO 9 and FICO 10

FICO 9 and FICO 10 treat paid collections as neutral. They ignore the account when they crunch your score. Pay a collection under one of these models and your score might rise because the negative weight disappears. Both also go lighter on unpaid medical collections compared to other types of debt, acknowledging that medical bills often come from situations you didn’t exactly plan for.

VantageScore 3.0 and 4.0

VantageScore 3.0 and 4.0 ignore all paid collections and disregard all medical collections, paid or unpaid, no matter the amount. If a lender’s using VantageScore 3.0 or 4.0, paying a non-medical collection wipes out its damage, and medical collections shouldn’t touch your score at all. VantageScore models are showing up more often with credit card issuers and they’re required for conforming mortgage loans by the end of 2025.

| Model | Treatment of Paid Collections |

|---|---|

| FICO 8 | Paid collections still penalize the score; no improvement after payment |

| FICO 9 / FICO 10 | Paid collections ignored; score may increase after payment |

| VantageScore 3.0 / 4.0 | All paid collections ignored; all medical collections ignored |

Timeline: How Long It Takes for Paid Collections to Update on Credit Reports

After you pay a collections account, the collector reports the updated status to Experian, Equifax, and TransUnion. Most collection agencies report updates once a month, so you’re looking at 30 to 45 days before the “paid” notation shows up on your reports. Some agencies move faster, especially if you ask for written confirmation and follow up, but 30 to 45 days is typical.

Your credit score might update as soon as the bureau processes the new info, but timing’s a bit of a lottery. If a lender pulls your credit the day before the update posts, they see the old unpaid status. Pull it the day after and they see it paid, and if they’re using a newer scoring model, maybe a higher score too. Check your reports about 60 days after payment to make sure everything landed correctly.

Four things affect how fast a paid collection updates:

- Reporting cycle – Most agencies report monthly, not right after you pay.

- Payment processing time – Electronic payments clear quicker than checks, which can take 7 to 10 business days.

- Agency policy – Smaller or regional agencies might report less often than the big national firms.

- Bureau processing delays – Each bureau runs on its own schedule, so one might show the change before the others do.

Paid vs. Unpaid Collections: Which Is Better for Your Credit Health?

Paying a collection is almost always better for your credit health than leaving it unpaid, even if your score doesn’t budge right away. A paid collection stops interest and fees from piling up, ends the endless calls and letters, and wipes out the risk of a lawsuit or wage garnishment. Plenty of lenders, especially mortgage lenders, won’t approve you until collections are paid, no matter what your score looks like.

An unpaid collection keeps damaging your profile in multiple ways. The account might get sold to a new collector, which restarts the whole circus and sometimes illegally resets the age of the debt. Unpaid collections can turn into legal judgments, letting collectors garnish your wages or slap liens on your property. Lenders reviewing your full report see an unpaid collection as a current obligation you’re ignoring, and that raises serious red flags about whether you can handle new debt responsibly.

Paid collections offer real advantages even under older scoring models that don’t immediately raise your score:

- Lenders approve applications more often when they see “paid” instead of “unpaid”

- Paying stops the debt from getting passed to more aggressive third-party agencies

- A paid collection can’t turn into a lawsuit or judgment

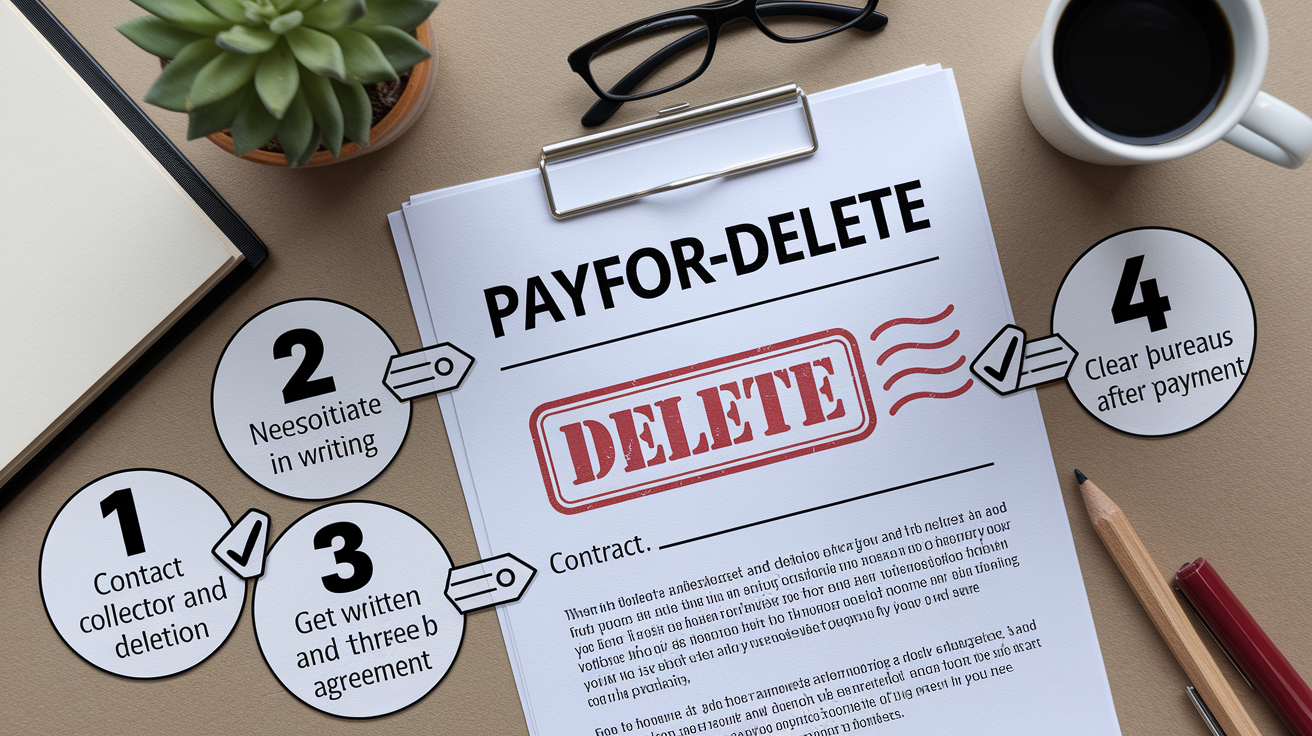

When Pay-for-Delete Is Possible and How It Works

Pay-for-delete is a deal where a collection agency agrees to remove the collection entry from your credit reports in exchange for full or partial payment. It’s not guaranteed and credit-reporting rules don’t require it, but some collectors offer it as a negotiation tool to get you to pay. Pay-for-delete works best with smaller agencies or original creditors who still own the debt, because they’ve got more flexibility than large debt buyers locked into strict corporate policies.

Credit bureaus don’t mandate pay-for-delete, but they let furnishers (the entities that report data) request deletion of any account whenever they want. If a collector agrees to delete the entry, they send an updated file to the bureaus marking the account as “delete” or “remove,” and the bureaus process it within 30 to 45 days. Pay-for-delete’s more common with debts under $1,000 and with collectors who want to close the account fast without going to court.

To request pay-for-delete, follow these steps:

- Contact the collector in writing – Send a letter or email proposing payment in exchange for deletion, and keep copies of everything.

- Negotiate the amount – Offer a lump sum or settlement amount, and ask for deletion as part of the deal.

- Get the agreement in writing before paying – Require a signed letter on company letterhead confirming they’ll request deletion after your payment clears.

- Verify deletion on your credit reports – Check all three bureaus 60 days after payment to make sure the collection’s gone.

Pay-for-delete isn’t available from every collector. Large agencies or those tied to investor contracts might refuse. If deletion’s off the table, negotiate to have the account marked “paid in full” instead of “settled for less than owed,” because some lenders view settled accounts as slightly worse.

Steps to Repair and Improve Your Credit After Resolving Collections

Once you’ve paid or settled a collections account, your next move is rebuilding your credit profile by adding positive payment history and knocking down other risk factors. Payment history’s the biggest piece of both FICO and VantageScore calculations (35% of FICO and 40 to 41% of VantageScore), so consistent on-time payments on current accounts start offsetting that old derogatory mark.

Start by pulling your credit reports from all three bureaus and checking for inaccuracies. If a collection shows as unpaid when you paid it, or the balance is wrong, file a dispute with the bureau reporting the error. Disputes get investigated within 30 days, and errors that can’t be verified have to be removed. Dropping your credit utilization ratio (the percentage of available credit you’re using) also packs a punch. Keep balances below 30% of your limits, ideally below 10% on revolving accounts like credit cards.

If your credit’s banged up and you’re having trouble qualifying for new credit, there are tools built to help you rebuild safely. A secured credit card requires a cash deposit that becomes your credit limit, and the issuer reports your on-time payments to the bureaus just like a regular card. Credit-builder loans hold the loan proceeds in a savings account while you make monthly payments, then release the funds to you at the end. Each payment gets reported and builds positive history. Becoming an authorized user on someone else’s well-managed credit card can help too, because their payment history might show up on your reports.

Six ways to improve your credit after resolving collections:

- Dispute inaccuracies – File disputes for any incorrect balances, statuses, or accounts that aren’t yours.

- Negotiate deletion if you can – Ask for pay-for-delete in writing before making any payment on remaining collections.

- Drop your utilization – Pay down credit card balances to below 30% of limits, and knock out small balances completely.

- Open a secured credit card – Use it for small purchases each month and pay the full balance on time to stack up positive payment history.

- Become an authorized user – Ask a family member with solid credit to add you to their account, making sure the issuer reports authorized users to all three bureaus.

- Monitor your reports monthly – Use free monitoring tools to catch new errors and track score changes as positive history builds up.

Final Words

In the action, paying a collection can help your score depending on the model, since newer scores like FICO 9/10 and VantageScore ignore paid collections while older models might not.

Paying still improves how lenders see you, can speed mortgage approval, and stops added fees. Updates usually show within 30 to 45 days, though it can take longer.

If you’re asking ‘does paying off a collections account improve credit score’, often the answer is yes under modern models — and it’s a solid step toward better credit.

FAQ

Q: How much does your credit score increase when you pay off collections?

A: Paying off collections can raise your credit score, but the change depends on the scoring model and your overall file — often a modest gain (tens of points); FICO 9/10 and Vantage ignore paid collections, older models may not.

Q: How to raise credit score 100 points in 30 days?

A: Raising your credit score 100 points in 30 days is rare but possible if you fix reporting errors, quickly lower credit card balances (utilization), have lenders report updates fast, or remove negative items via negotiation.

Q: Can you have a 700 credit score with paid collections?

A: You can have a 700 credit score with paid collections if the rest of your credit looks strong — FICO 9/10 and Vantage often ignore paid collections, though older models or some lenders might still view them negatively.

Q: What is the biggest killer of credit scores?

A: The biggest killer of credit scores is missed or late payments — payment history matters most. High credit card balances (high utilization) are the next biggest damage and can lower scores quickly.