{kind=link}

Think you can get an auto loan without the right paperwork?

Missing or sloppy documents are the number one reason applications stall or get denied.

Lenders use underwriting files to confirm who you are, how much you earn, where you live, the car’s value, and that you have insurance.

This post walks through the exact documents lenders require for auto loan underwriting success, what you need for preapproval, what you need to close, and simple steps to organize everything so your loan moves quickly.

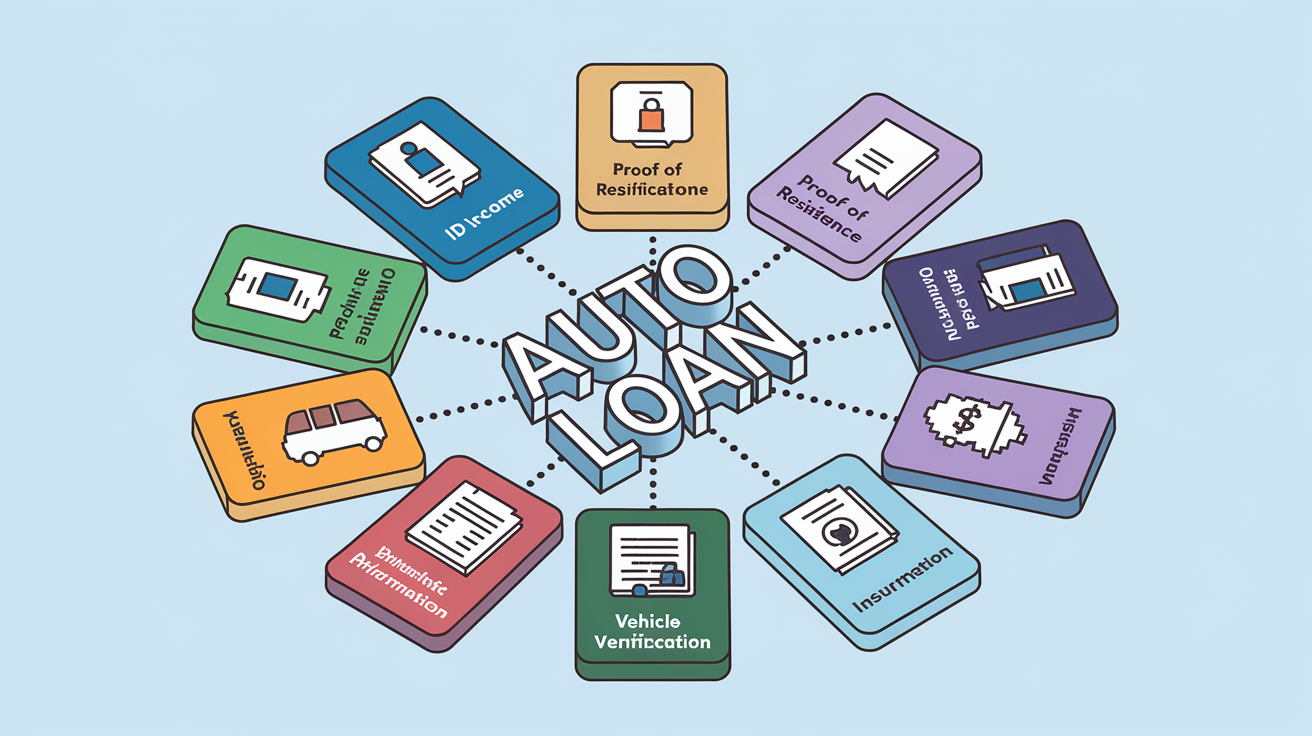

Auto Loan Application Documents Checklist (Quick Overview)

Lenders use underwriting documents to confirm who you are, whether you can actually afford the payments, and that the car you’re buying is worth what you’re paying. Missing or sloppy paperwork? That’s the number one reason applications get stuck or denied. Knowing what you need before you hit submit gives you time to track down anything that’s missing.

Most lenders want these categories:

- Proof of income (recent pay stubs, W-2s, tax returns, or bank statements)

- Government-issued photo ID (driver’s license or passport)

- Proof of residence (utility bill, lease, or bank statement from the last month or two)

- Employment info (employer name, contact, how long you’ve been there)

- Credit authorization (signed form so they can pull your report)

- Vehicle details (VIN, year, make, model, mileage, purchase agreement)

- Down payment verification (bank statement or trade-in appraisal showing you’ve got the cash)

- Proof of insurance (declarations page listing the lender as lienholder, with full coverage)

Preapproval usually needs just income and ID. Final approval and funding? You’ll need everything, including insurance and vehicle paperwork.

Detailed Breakdown of Each Required Document Category

Proof of income tells the lender you earn enough to handle the monthly payment. If you’re salaried, bring your two most recent pay stubs (covering at least 30 days) and the last two years of W-2s. If your stubs don’t show year-to-date totals or your income changes month to month, expect them to ask for one to three months of bank statements. Self-employed? You’ll need two years of complete federal tax returns with all schedules, a recent profit-and-loss statement, and business bank statements.

ID verification confirms your legal identity and makes sure your name matches your credit file. A current driver’s license or passport works. The name on your ID has to match the name on your application and credit report. Recently changed your name? Bring proof like a marriage certificate or court order.

Proof of residence verifies your physical address for lien and title paperwork. You can use a utility bill, bank statement, lease, or mortgage statement dated within the last 30 to 60 days. The address needs to match your license or credit report. PO boxes don’t count. Just moved? Provide a signed lease or closing statement plus a recent piece of mail at the new address.

Employment confirmation helps the lender check job stability and verify the income you listed. You’ll give them your employer’s name, address, and HR or payroll contact info. Some lenders send a verification of employment form directly to your employer. Started a new job recently? Submit your signed offer letter with your start date and salary.

Credit authorization forms give the lender permission to pull your credit report and review your history. You’ll sign this when you submit your application, either online or on paper. They’ll use your full Social Security number and date of birth to run the check.

Vehicle information documents prove the car’s identity, value, and ownership status. You’ll need the VIN, year, make, model, trim, and current mileage. Buying new? The dealer provides a purchase agreement or bill of sale showing the sale price and your down payment. Trading in or refinancing? Submit the current title listing any lienholders and the registration. Private sale? You’ll need an odometer statement and bill of sale signed by the seller.

Down payment verification confirms you’ve got the cash or trade-in equity you claimed on your application. Lenders want bank statements showing the account name, number, and available balance. Getting gift money? You’ll need a signed gift letter with the donor’s name, relationship, Social Security number, and the amount. Trade-in appraisals and title documents count as down payment proof when you’re using equity from another vehicle.

Insurance requirements protect the lender’s collateral. Before they fund the loan, you have to provide a declarations page or insurance binder showing full coverage (comprehensive and collision, plus your state’s liability minimums). The policy has to be effective on or before the funding date and list the lender as the lienholder, with the lender’s exact legal name and mailing address. Your insurance card or binder should show your name, the insurer’s name and NAIC number, the policy number, and the effective and expiration dates.

How Documentation Requirements Vary by Lender Type

Banks and national online lenders tend to be the strictest. They usually want two years of W-2s or tax returns, recent pay stubs, and bank statements even if your credit’s solid. Self-employed? Expect to hand over complete tax returns with all schedules, profit-and-loss statements, and several months of business and personal bank statements. Banks often want original signatures on certain documents and rarely accept alternative income verification. Their underwriting timelines run anywhere from 24 to 72 hours after they get everything.

Credit unions mostly follow the same playbook as banks but add membership verification steps. You’ll need to prove eligibility by showing employment with a qualifying organization, residence in a specific area, or membership in an affiliated group. Some credit unions accept fewer income documents for longtime members with perfect payment histories. Others waive residence or employment verification if your direct deposit and account history are already in their system.

Dealership financing and captive lenders (manufacturer-owned finance arms) sometimes streamline paperwork for customers with good to excellent credit. They might accept a single recent pay stub or offer stated-income approval without W-2s if your credit score’s high enough. But subprime dealer programs often demand larger down payments (10 to 20 percent or more), additional asset verification, and more detailed explanations for recent credit problems. Dealer finance departments handle most vehicle documentation directly, but you still have to provide ID, income proof, residence verification, and insurance before the lender releases funds.

Special Documentation Requirements for Self‑Employed Applicants

Self-employed borrowers and freelancers face higher documentation standards because lenders can’t verify income with a simple pay stub. You’ll generally need to show consistent, documentable earnings over at least two years.

Typical documents lenders request from self-employed applicants:

- Last two years of complete federal tax returns (Form 1040 plus all schedules, especially Schedule C for sole proprietors or Schedule K-1 for partnership/S-corp income)

- Year-to-date profit-and-loss statement, signed and dated

- Two to three months of business bank statements showing deposits and operating expenses

- Two to three months of personal bank statements

- 1099 forms for the last two years (if you get them)

- Business license, IRS acceptance letter, or articles of incorporation (for recently formed businesses)

Lenders review these to calculate your stable monthly income, which is often lower than your gross revenue once they account for business expenses and tax deductions. Underwriters might average your last two years of net self-employment income and divide by 24 to estimate a monthly figure. If your income’s been climbing, some lenders will use the more recent year instead. Providing clear, organized tax returns and a current profit-and-loss statement helps underwriters see the trend and cuts down on extra verification requests that slow everything down.

Tips for Organizing and Submitting Your Auto Loan Documents Successfully

Gathering your documents ahead of time prevents last-minute scrambling and speeds up underwriting. Most lenders accept digital uploads, so scan or photograph each document as a clear, legible PDF or JPEG. Label your files with specific names and dates, like “Paystub2026-03-15.pdf” or “BankStatementFebruary2026.pdf” instead of generic names like “Document1.pdf.” Create a single folder or zip file per lender application and include a simple cover sheet listing your full name, date of birth, and loan reference number if the lender gave you one.

Keep both digital and physical copies for your records. If the lender needs original signatures or title documents for funding, bring the originals plus two photocopies to the closing appointment.

Steps to organize and submit your auto loan documents without delays:

- Check expiration dates. Make sure your driver’s license, insurance card, and any employment offer letters are current and won’t expire before your loan closes.

- Verify name and address consistency. Your legal name and address should match across your ID, credit report, pay stubs, and residence proof. Discrepancies cause verification delays.

- Redact only unnecessary sensitive data. You can black out full account numbers on statements you share for initial review, but be ready to provide unredacted originals when the lender requests them for final verification.

- Respond to lender requests immediately. If underwriting asks for a missing document or a letter of explanation, submit it the same day to avoid pushing your approval into the next business week.

- Confirm receipt. After uploading or emailing documents, follow up with the lender to confirm they received everything and ask if any items need clarification or resubmission.

Final Words

In the action, we ran through a quick checklist and then unpacked each item—proof of income, ID, residence, employment, credit consent, vehicle papers, down payment proof, and insurance.

You saw how banks, credit unions, and dealer financing differ, what self‑employed borrowers need, and simple steps to organize and submit files so underwriting moves faster.

Keep a one‑place folder, scan clear copies, and double‑check dates and numbers. Knowing the documents lenders require for auto loan underwriting helps you finish faster and avoid delays. You’re set to apply with more confidence.

FAQ

Q: What documents do you need to be approved for a car loan?

A: The documents you need to be approved for a car loan are proof of income (pay stubs or tax returns), photo ID, proof of residence, employment details, credit authorization, vehicle info (VIN, purchase agreement), down payment proof, and insurance.

Q: What is the underwriting process for a car loan?

A: The underwriting process for a car loan is verifying your income, identity, residence and employment, pulling your credit, checking debt-to-income (DTI), confirming vehicle details, and deciding loan terms and final approval.

Q: What disqualifies you from an auto loan?

A: Factors that can disqualify you from an auto loan are very low credit scores, insufficient or undocumented income, high DTI (debt compared to income), recent bankruptcy, missing or inconsistent documents, lack of required insurance, or title problems.

Q: What do lenders look for when applying for a car loan?

A: Lenders look for steady income, a solid credit score, low DTI (debt compared to income), stable employment and residence, a reasonable down payment, vehicle value and condition, required insurance, and accurate verification documents.