{kind=link}

Think a lender’s approval means you can afford the payment?

Not true.

Lenders use DTI (debt compared to your income) to say yes, but your take-home budget shows what you can actually pay each month.

This post gives a clear, step-by-step way to estimate an affordable monthly loan payment by combining your DTI and real household budget.

You’ll learn how to pick a target DTI, subtract current debts, and turn the leftover into a monthly payment and loan amount that won’t wreck your cash flow.

Establishing an Affordable Loan Payment Using DTI and Budget Calculations

Lenders approve you based on debt-to-income ratio, but your monthly budget tells you what you can actually afford. DTI measures how much of your gross monthly income already goes to recurring debt payments. Front-end DTI looks at just your housing cost (the projected mortgage payment including property taxes, homeowners insurance, and mortgage insurance). Back-end DTI includes that housing payment plus every other monthly debt: car loans, student loans, credit cards, personal loans, alimony, and child support. Lenders care more about the back-end number because it shows your total debt load.

Most lenders want a front-end DTI under 28% and a back-end under 36%. Plenty of mortgages close around 40%. FHA guidelines allow up to 43% (sometimes 57% if you’ve got big savings or rock-solid income). USDA caps at 41%, and VA lenders start asking hard questions above 41%. Approval gets tough when your DTI climbs past 50%. If your numbers push into that zone, you’re carrying too much debt for most lenders to say yes.

Here’s how to combine DTI limits and your real household budget to estimate a safe maximum monthly loan payment:

Calculate your gross monthly income. Add up your salary, hourly pay, regular bonuses, and any recurring income before taxes or deductions. Divide annual income by 12 if you’re paid yearly.

List all current monthly debt obligations. Write down the minimum payment for every credit card, the monthly amount for car loans, student loans, personal loans, and any alimony or child support. Don’t include utilities, groceries, or one-time expenses.

Calculate your front-end and back-end DTI. Front-end is your projected loan payment (including taxes and insurance if it’s a mortgage) divided by gross income. Back-end is that same payment plus all your other monthly debts, divided by gross income. Multiply each result by 100 to get a percentage.

Pick a target back-end DTI. Use 36% if you want a conservative cushion. If you’ve got strong credit and stable income, you can stretch to 40% or 43%, but know that you’re closer to lender limits.

Solve for your maximum new loan payment. Multiply your gross monthly income by your target DTI percentage to get the total dollars you can spend on debt each month. Subtract your current monthly debt payments. What’s left is the most you should commit to a new loan payment.

Step-by-Step Conversion of Payment Capacity Into Loan Principal

Once you know how many dollars you can safely spend each month on a new loan, you need to convert that payment capacity into a loan amount. The loan principal you can afford depends on three things: the monthly payment you have room for, the interest rate (APR), and the number of months you’ll take to repay.

Here’s the procedure:

Confirm your monthly payment capacity. Use the number you found in the previous section (your target DTI times gross income, minus current debts).

Choose a loan term in months. Common terms are 36 months, 60 months, 120 months (10 years), 180 months (15 years), or 360 months (30 years). Shorter terms mean higher monthly payments but less total interest.

Determine the monthly interest rate. Take the annual percentage rate (APR) the lender quotes and divide by 12. For example, 7% APR becomes 0.07 ÷ 12 = 0.00583 per month.

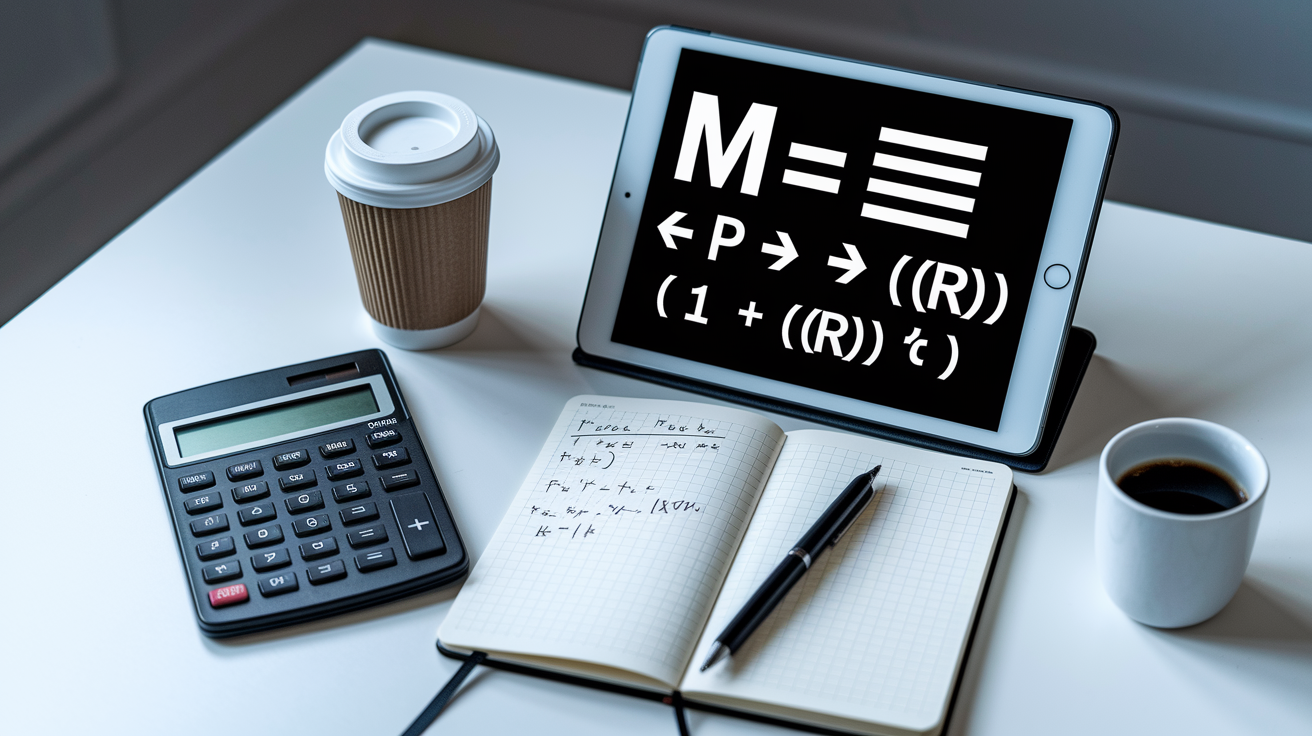

Apply the amortization formula. The formula to find principal P when you know the monthly payment M is: P = M × (1 − (1 + r)^−n) / r, where r is the monthly interest rate and n is the number of months.

Calculate the resulting principal. Plug your numbers into the formula or use an online loan calculator that lets you enter payment, rate, and term to solve for principal.

Quick example: You’ve got $800 per month available for a new loan payment. The lender offers 7% APR for a 60-month personal loan. Monthly rate r = 0.07 ÷ 12 = 0.00583. Principal P = 800 × (1 − (1.00583)^−60) / 0.00583 ≈ $40,150. That $800 monthly payment will let you borrow about $40,000 at 7% over five years.

If you shorten the term to 36 months at the same rate, the same $800 payment buys you about $26,600 in principal. Longer terms let you borrow more, but you pay more interest over the life of the loan.

Using Budget Analysis to Confirm a Realistic Monthly Loan Payment

DTI uses your gross income and counts only recurring debt payments. It ignores rent (if you’re not buying a home yet), utilities, groceries, gas, insurance premiums, childcare, and every other real expense that hits your checking account each month. A payment that looks fine by DTI math can still wreck your budget if it leaves you short on take-home pay.

Check affordability with a simple budget worksheet. Start with your monthly take-home income (net pay after taxes, retirement contributions, and insurance). Subtract your fixed monthly expenses: rent or current mortgage, utilities, car insurance, groceries, transportation, phone, internet, and minimum debt payments. Then subtract variable costs like gas, subscriptions, and entertainment. Finally, set aside money for your emergency fund or short-term savings. What’s left is your true cushion. If your proposed new loan payment eats into that cushion or forces you to skip savings, the payment is too high even if your DTI says you qualify.

Budget worksheet fields to fill in:

Gross monthly income: Pay before deductions

Net monthly income: Actual take-home after taxes and withholding

Current recurring debt payments: Student loans, credit cards, car loan, any other monthly minimums

Essential living expenses: Rent or mortgage, utilities, groceries, insurance, transportation, childcare

Discretionary spending: Subscriptions, dining out, hobbies, entertainment

Proposed new loan payment: The monthly amount you’re testing

Add up current debt payments and the proposed new payment, then add all essential and discretionary expenses. If that total exceeds your net income, you’re overextended. If it leaves less than $200 to $300 for unexpected costs or short-term goals, you’re at risk of payment shock, that stress that hits when a new monthly obligation crowds out flexibility. Adjust the proposed payment down until you see a buffer that feels safe.

Worked Examples: Calculating Affordable Monthly Loan Payments

Example 1: Mortgage payment estimation

You earn $7,000 gross per month. Current debts: $350 car payment, $250 student loan, $200 credit card minimums. Total existing debt = $800/month. You want to buy a house and you’re targeting a back-end DTI of 36%.

Max allowable total debt = $7,000 × 0.36 = $2,520 per month.

Available for mortgage payment = $2,520 − $800 = $1,720 per month.

You find a lender quoting 6.5% APR on a 30-year fixed mortgage. Monthly rate r = 0.065 ÷ 12 = 0.00542. Term n = 360 months.

Principal P = 1,720 × (1 − (1.00542)^−360) / 0.00542 ≈ $272,000.

At 6.5% over 30 years, a $1,720 monthly payment (principal and interest only) supports roughly a $272,000 mortgage. Remember that your actual housing payment will include property taxes, homeowners insurance, and possibly mortgage insurance, so your true affordable home price is lower. If taxes and insurance add $400 per month, your principal and interest budget drops to about $1,320, which supports roughly $209,000 in loan principal.

Example 2: Auto loan payment capacity comparison

Same borrower, $7,000 gross monthly income, $800 existing debt. You decide to finance a car instead. You keep the 36% DTI target, so you have $1,720 available monthly. The dealer offers 7% APR.

Option A: 60-month term (5 years).

Monthly rate r = 0.07 ÷ 12 = 0.00583, n = 60.

Principal P = 1,720 × (1 − (1.00583)^−60) / 0.00583 ≈ $86,300.

Option B: 36-month term (3 years).

Same rate, n = 36.

Principal P = 1,720 × (1 − (1.00583)^−36) / 0.00583 ≈ $56,000.

The 60-month term lets you borrow about $86,000, but you’ll pay thousands more in interest. The 36-month term caps you at $56,000 but you own the car faster and pay less total interest. If a $1,720 monthly payment feels too tight on your net budget, drop the payment to $600 per month and recalculate. 60 months at 7% supports about $30,000 principal, 36 months supports about $19,500.

Identifying Warning Signs Your Estimated Monthly Payment Is Too High

Even if your DTI math says a payment fits, watch for red flags that the number is pushing you past safe limits. A back-end DTI above 43% puts you in the zone where most lenders apply extra scrutiny or decline your application. Above 50%, approval is rare unless you bring huge compensating factors like a massive down payment or co-signer.

Five warning signs you’re overextended:

Your back-end DTI exceeds 43%. You’re at or past the upper guideline for many loan programs, and you’ll face higher interest rates or denial.

You’re cutting essential expenses to make room. If covering the proposed payment means skipping groceries, gas, or medical copays, the payment isn’t affordable.

You have no emergency fund. A safe monthly payment leaves room to save $100 to $200 each month. If the new loan wipes out savings capacity, one unexpected car repair or medical bill will force you onto credit cards.

You’re already missing payments on existing debt. Adding a new monthly obligation when you can’t consistently pay current bills guarantees trouble.

Your net cashflow after the payment is zero or negative. Run the budget worksheet. If your take-home income minus all expenses (including the proposed payment) is less than zero, you cannot afford the loan.

If any of these apply, reduce the loan amount, extend the term to lower the monthly payment, or wait and pay down existing debt before borrowing.

Improving Your DTI to Increase Affordable Monthly Payment Capacity

Lowering your DTI opens up more room for a new loan payment and improves your approval odds. The formula is simple: reduce monthly debt obligations, increase gross income, or both. Even small moves can shift your DTI by several percentage points and free up hundreds of dollars in monthly capacity.

Paying off one loan makes an immediate impact. If you carry a $300 personal loan payment and your total monthly debt is $1,000 on $5,000 gross income, your DTI is 20%. Pay off that $300 loan and your debt drops to $700, new DTI is 14%. That six-point improvement can be the difference between approval and denial, or between a 7% rate and a 6% rate.

Small Actions That Quickly Improve DTI

Pay off the smallest balance first. Eliminate a $150 credit card minimum or a $200 furniture loan. Each monthly payment you remove drops your DTI and frees capacity for the new loan.

Avoid opening new credit before applying. Every new account adds a monthly minimum to your back-end DTI, even if the balance is zero. Wait until after your loan closes.

Increase your income. A raise, promotion, consistent overtime, or side income all boost your gross monthly income and lower your DTI percentage without changing your debt load.

Refinance or consolidate high-rate debt. Combining multiple credit card payments into one lower-interest personal loan can reduce your total monthly obligation, improving DTI and freeing cash for the new payment.

Lenders also consider compensating factors. If your DTI is 44% but you’ve got $50,000 in savings, stable employment for five years, and no other red flags, some lenders will approve you at a higher ratio. Strong credit, low loan-to-value, and significant assets give you room to stretch DTI limits. But don’t rely on exceptions. Prioritize bringing your ratio under 36% before applying.

Tools and Formulas to Estimate Monthly Loan Payments Accurately

The math you need is straightforward, but calculators save time and catch mistakes. Use the standard amortization formula to convert principal, rate, and term into a monthly payment, or rearrange it to solve for principal when you know the payment you can afford.

Monthly payment formula: M = P × r(1 + r)^n / ((1 + r)^n − 1), where P is the loan principal, r is the monthly interest rate (annual APR ÷ 12), and n is the number of months.

Principal formula (when you know the payment): P = M × (1 − (1 + r)^−n) / r.

Three types of tools to use:

Online loan calculators. Enter principal, APR, and term to get the monthly payment, or enter the payment you can afford to solve for principal. Most bank and credit union websites offer free calculators.

Spreadsheet amortization templates. Download a simple Excel or Google Sheets template that shows month-by-month principal, interest, and balance. Adjust the inputs to test different scenarios.

DTI worksheets. Print or build a one-page form listing gross income, each monthly debt, target DTI percentage, and available payment capacity. Recalculate every time your income or debts change.

Run multiple scenarios. Compare a 60-month loan at 7% against a 48-month loan at 6.5%. Check how a $10,000 principal at different rates changes your monthly obligation. The more you model, the clearer your true affordable payment becomes. Plug your final number into your budget worksheet and confirm that your net income, after all expenses and the new payment, still leaves $200 to $300 for surprises and short-term savings.

Final Words

in the action we walked through using DTI limits and a household budget to set a safe maximum payment. We showed front-end vs back-end ratios, the 28/36 targets and the 43% upper bound.

Then we turned that monthly capacity into a loan amount, checked it against take-home pay and payment shock, ran worked examples, and listed red flags plus quick ways to lower DTI.

Use this guide to learn how to estimate an affordable monthly loan payment using DTI and budget, run the numbers, and adjust until it fits your life. You’ll be more confident and ready to shop smart.

FAQ

Q: What is the 33% mortgage rule?

A: The 33% mortgage rule is a guideline saying your monthly housing payment (including taxes and insurance) should be about 33% of your gross monthly income to stay affordable.

Q: How to calculate affordable monthly payment?

A: To calculate an affordable monthly payment, combine DTI limits and your household budget: use gross income, list debts, compute front‑end and back‑end DTI, then set the max payment that fits both.

Q: What are common DTI mistakes?

A: Common DTI mistakes include using net income instead of gross, forgetting recurring debts, double‑counting payments, ignoring taxes/insurance in front‑end, and not checking lender‑specific thresholds.

Q: Is a 20% DTI good?

A: A 20% DTI is generally good; it’s well below common targets (front‑end 28%, back‑end 36%) and makes loan approval easier while leaving more room for monthly expenses.