{kind=link}

Should you pay points to lower your mortgage rate, or are you just handing money to the lender?

Points (each equals 1% of your loan) are paid at closing to buy down your rate—often about 0.25% per point.

The key is the break-even (months it takes to recoup the upfront cost).

Thesis: paying points makes sense when your break-even is shorter than how long you’ll keep the loan, you have spare cash after closing, and you don’t plan to refinance soon.

Understanding Mortgage Points and Quick Break-Even Basics

Mortgage points are an upfront fee you pay at closing to buy down your interest rate. Each point costs 1% of your loan amount. So on a $300,000 mortgage, one point runs you $3,000. Lenders usually knock about 0.25% off your rate for each point you buy, though the exact reduction depends on the lender and what’s happening in the market.

The real question is how long it takes to get that upfront money back through lower monthly payments. That’s your break-even period. If you drop $3,000 on one point and save $50 a month on your payment, you’ll break even in 60 months. Five years. If you’re planning to keep the home and the loan longer than that, buying points can cut thousands off your total interest bill.

Here’s the math:

- Multiply your loan amount by the number of points to get what you’ll pay upfront. $300,000 × 0.01 = $3,000 for one point.

- Figure out the difference between your monthly payment without points and your payment with the lower rate.

- Divide what you paid upfront by your monthly savings. That’s how many months until you break even.

Detailed Break-Even Analysis for Paying Points

The basic formula’s simple enough, but the actual value depends on your loan size and how much rate reduction your lender’s offering per point. Bigger loans make both the cost and the savings bigger. A 0.25% rate drop on a $500,000 mortgage saves way more each month than the same cut on a $200,000 loan, even though you’re paying one point either way.

Most lenders give you rate sheets showing different scenarios with varying point amounts and the rates you’d get. You can run the numbers yourself with any mortgage calculator. Plug in your loan amount and term, then compare the monthly principal and interest at your base rate versus the rate after buying points. The monthly difference is what you save, and dividing your upfront cost by that monthly savings tells you your break-even in months.

| Loan Size | Cost of One Point | Monthly Savings (approx.) | Break-Even Months |

|---|---|---|---|

| $200,000 | $2,000 | $30 | 67 |

| $300,000 | $3,000 | $50 | 60 |

| $400,000 | $4,000 | $65 | 62 |

| $500,000 | $5,000 | $80 | 63 |

Situations Where Paying Points Usually Makes Sense

Buying points works when you’re planning to stay in the home for a long time and keep the mortgage for years past your break-even. If you’re expecting to live there for ten years and your break-even hits at five, you get five full years of monthly savings at no extra cost. Over a 30-year loan, those savings add up to a lot less total interest.

Points also make sense when you’ve got enough cash that paying a few thousand upfront won’t wipe out your emergency fund or leave you scrambling for closing costs, moving expenses, or immediate repairs. If your finances are solid and you’re confident you won’t refinance anytime soon, the upfront investment pays off.

Another scenario where points work well is when interest rates are holding steady or expected to climb. Locking in a lower rate now by buying points protects you from future rate increases and cuts the odds you’ll want to refinance before you’ve recouped your cost. In strong housing markets where you’re buying what you hope is a forever home, points can be a smart long-term bet.

Situations Where Paying Points Usually Doesn’t Make Sense

Paying points is a bad move if you’re planning to sell within a few years. If your break-even is five years but you expect to relocate in three, you’ll lose money on the upfront cost without seeing the long-term benefit.

Points don’t work if you’re planning to refinance soon. If rates are dropping or you expect your credit to improve enough to snag a better rate in a year or two, you’ll refinance before breaking even and the money you spent on points is gone. Same deal if you’re getting an adjustable-rate mortgage and planning to refinance before the fixed period ends.

If cash is tight, skip the points. Using every dollar you have to buy down your rate can leave you stuck if unexpected expenses pop up right after closing. Better to keep some liquidity for emergencies, home repairs, or other priorities than to lock cash into a rate reduction you might never fully benefit from.

Numerical Examples Comparing With and Without Points

Let’s look at a real comparison. Say you’ve got a $350,000 loan on a 30-year fixed mortgage. The base rate without points is 6.00%, giving you a monthly principal and interest payment of about $2,098. You buy one point for $3,500, and the lender drops your rate to 5.75%. Your monthly payment falls to roughly $2,041. That’s $57 in monthly savings.

Your break-even on that one point is $3,500 divided by $57, which comes out to about 61 months. Just over five years. If you buy two points for $7,000, your rate might drop to 5.50%, lowering your payment to around $1,987 and saving you about $111 per month. Break-even is $7,000 divided by $111, or roughly 63 months.

| Rate | Monthly Payment | Upfront Cost | Lifetime Interest Paid |

|---|---|---|---|

| 6.00% (no points) | $2,098 | $0 | $405,280 |

| 5.75% (one point) | $2,041 | $3,500 | $384,760 |

| 5.50% (two points) | $1,987 | $7,000 | $365,320 |

Factors That Influence Whether Points Are Worth It

Several things determine whether buying points will actually pay off. You need to look at them together, not one at a time.

Loan size: Bigger loans mean you pay more per point, but you also save more each month. On a $200,000 loan, one point costs $2,000. On a $500,000 loan, it’s $5,000. The savings scale the same way, so the break-even period stays pretty similar.

Interest rate environment: When rates are low, the value of buying points goes up because you’re locking in a historically good rate for the long haul. When rates are high and likely to fall, points become riskier since you’ll probably refinance before breaking even.

Expected homeownership period: The longer you plan to stay, the more time you have to recoup your upfront cost and enjoy those monthly savings. If you’re not sure you’ll be in the home for five years, points are a gamble.

Cash reserves and liquidity needs: If you’ve got plenty of savings and the upfront cost won’t strain your budget, points are easier to justify. If cash is tight or you’ve got better uses for the money, keep your liquidity and skip the points.

Your credit profile matters too. If your score’s borderline and you’re already getting a higher base rate, the rate reduction per point might be smaller or cost you more. Ask your lender exactly how much rate reduction you’ll get before you commit.

Opportunity Cost of Buying Mortgage Points

Every dollar you spend on points is a dollar you can’t use somewhere else. If you’ve got $5,000 available at closing, you could buy points to lower your mortgage rate. Or you could put that money into an investment account, pay down high-interest debt, or keep it in an emergency fund. Which option gives you the best return?

If you can earn more by investing the money than you save by lowering your rate, points are the wrong choice. Say buying a point saves you an effective annual return of 4%, but you could invest the same money in a diversified portfolio with an expected long-term return of 7%. Investing wins. Same logic applies to high-interest debt. If you’re carrying credit card balances at 18% interest, paying those down beats a 4% effective savings on your mortgage every time.

On the flip side, mortgage interest savings are guaranteed and risk-free, while investment returns bounce around. Some people prefer the certainty of a lower monthly payment and reduced lifetime interest, especially if they’re risk-averse or already maxing out retirement accounts with no high-interest debt hanging around. The right choice depends on your situation, risk tolerance, and what else you could do with the cash.

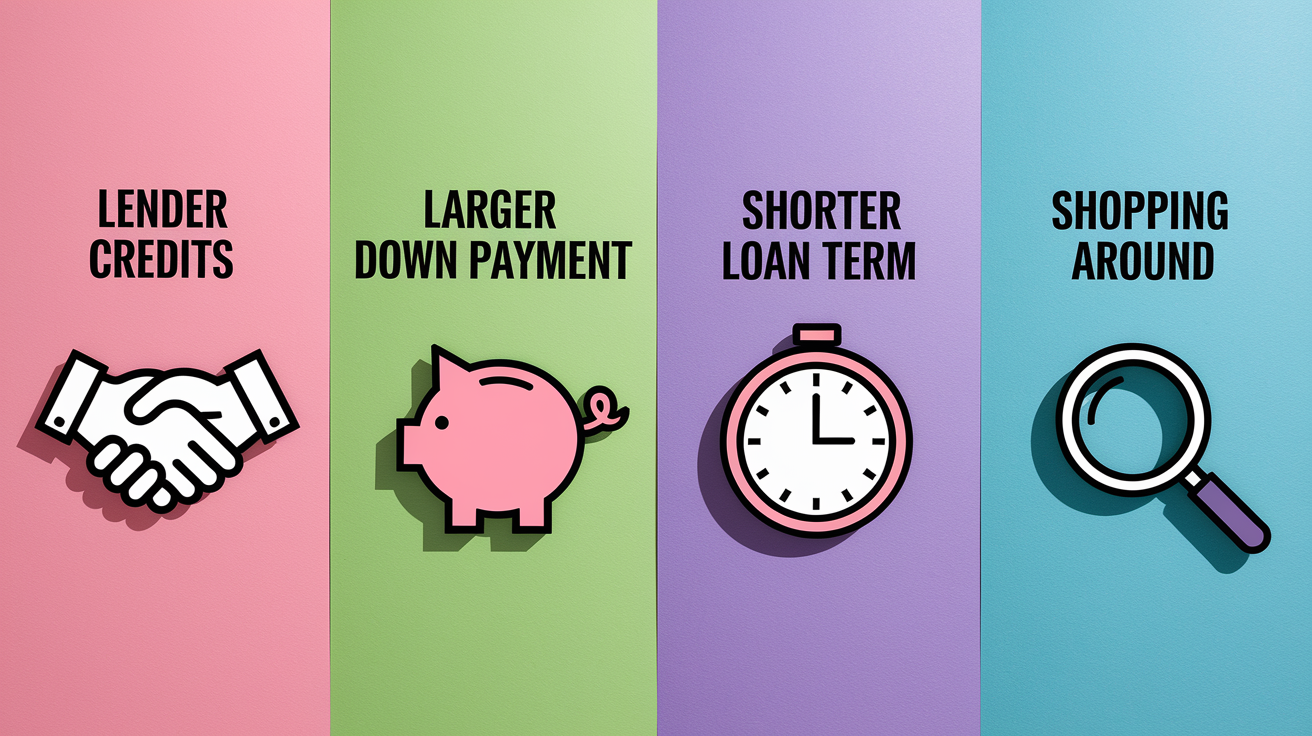

Alternatives to Paying Points

If you’re not sure about buying points, there are other ways to lower your mortgage costs or improve your position at closing. Each has trade-offs, but they’re worth comparing.

Lender credits: Some lenders offer a higher interest rate in exchange for covering some or all of your closing costs. This is the opposite of buying points. You pay nothing upfront, but your monthly payment and total interest go up.

Larger down payment: Putting more money down shrinks your loan amount, which lowers your monthly payment without paying points. It can also help you qualify for a better base rate or dodge private mortgage insurance.

Shorter loan term: A 15-year or 20-year mortgage usually comes with a lower interest rate than a 30-year loan. Your monthly payment will be higher, but you’ll pay way less total interest and own the home faster.

Shopping multiple lenders: Different lenders offer different base rates and point pricing. One lender might give you 5.75% with no points while another charges a point for the same rate. Always compare at least three lenders on identical terms.

Timing your purchase or refinance can matter too. If rates are expected to drop soon, waiting a few months might get you a better base rate without paying points. If rates are climbing, locking in now and buying points could protect you from higher costs down the road.

Final Words

in the action, we explained what mortgage points are, how each point often costs about 1% of the loan and can cut the rate by roughly 0.25%, and showed a simple break-even formula.

Next, we walked through detailed break-even math, real scenarios where points help or don’t, the opportunity cost, and practical alternatives like lender credits or shorter terms.

If you’re still asking “should I pay points to lower mortgage interest rate”, run the break-even on your numbers, compare options, and pick the choice that saves you most over the time you plan to stay. You’ll feel more confident.

FAQ

Q: Is it better to pay points for a lower interest rate?

A: Paying points for a lower interest rate is better when you plan to stay in the home long enough to recoup the upfront cost, have spare cash, and the break-even period is shorter than your expected ownership.

Q: How much do 2 points reduce the mortgage rate?

A: Two points typically reduce the mortgage rate by about 0.5% (about 0.25% per point), though the exact reduction varies by lender and market conditions.

Q: What is the 3 7 3 rule in mortgage?

A: The 3 7 3 rule in mortgage isn’t a universal standard; it’s often lender-specific jargon. Ask the lender to explain, and use a break-even calc instead: point cost divided by monthly savings.

Q: Is a 0.25% interest rate reduction worth it?

A: A 0.25% interest rate reduction is worth it if the upfront cost pays back before you move or refinance; larger loans and longer stays make small rate cuts more valuable.